.webp)

If you are an energy buyer reading about the Greenhouse Gas Protocol updating its Scope 2 standard, you may be worried about what it means for your renewable energy claims and your next Power Purchase Agreement (PPA).

The Greenhouse Gas Protocol's Technical Working Group has put forward three proposed changes to the market-based method: an hourly matching requirement, a deliverability requirement, and a complementary metric called Marginal Emissions Impact. The first public consultation period closed on 31 January 2026 with over 400 responses received. A second consultation runs in 2026. Reporting frameworks like SBTi, CDP, and CSRD will layer their own transition periods on top.

The proposals are set to tighten how Scope 2 greenhouse gas emissions are accounted for. However, they do not move corporate procurement targets, and they will not require any specific hourly matching target next year. The initial shift is to carbon accounting, not yet to procurement.

"It’s hourly accounting, not 100 per cent matching."

– Carolyn Addy, Renewabl, on the Plugged In Podcast

Energy buyers need to show how their demand lines up with their procurement, hour by hour. That work sits below the standard, in the data layer most corporates have been postponing. The buyers who use the next 18 months on data readiness get two returns from a single project: a more defensible Scope 2 claim, and a sharper view of how their next PPA actually hedges their load.

What we hear from corporate energy and sustainability leads

We have analysed our conversations with more than 100 corporate energy buyers over the past year. The most common worry is the complexity the revision will add to a function that is already stretched.

"We are extremely worried because of the complexity, the complexity that is going to add to our daily life."

– Sustainability and energy lead, global agri-business

Most energy and sustainability teams are lean for the size of portfolio they cover. A team of one or two people running hundreds of sites is not unusual.

Two things worth saying clearly:

1. First, the revision does not introduce a new procurement target. It asks you to read the data you already have on an hourly basis rather than an annual one.

2. Second, the change is phased over several years, with feasibility adjustments for buyers without hourly meter data yet.

The reason to start the data work this year is procurement timing – PPA cycles run two to three years, and the standard publishes within that period. The cliff edge people are bracing for does not exist.

What is actually being proposed (and what is not)

The proposed changes raise the bar on the eight Scope 2 Quality Criteria already inside the existing GHGP Guidance – the rules a contractual instrument has to meet for its emissions claim to count under the market-based method.

Two of the eight carry most of the weight in the revisions: time matching and geographic deliverability. The other six – ownership, exclusivity, no double counting, vintage, the operating period, and the deliverability link itself – tighten around them.

The three proposed elements:

- Hourly matching. Any contractual instrument used in the market-based method would need to be matched to consumption on an hourly basis.

- Deliverability. The clean energy generation being claimed has to sit inside the same electrical region as the consumption – typically a bidding zone, country, or balancing area – unless a direct contract or a physical delivery link demonstrates the power could have reached the load.

- Marginal Emissions Impact. A complementary metric proposed in parallel by the Scope 2 Working Group. It sits alongside the inventory rather than replacing it, and asks whether a given purchase actually displaces fossil generation at the margin – rather than adding clean MWh to a system that would have absorbed them anyway.

.webp)

One thing the proposal does not do: require 100 per cent hourly matching. A good deal of the opposition circulating in the market is premised on the assumption that 100 per cent is the only way to comply. The draft standard does not say that. A company that reaches 70 per cent hourly coverage reports a 70 per cent score – it does not fail a compliance test. Smaller organisations keep access to the annual method.

The case for granular matching is straightforward: the hours when renewable supply is scarce are when electricity grids carry the highest emissions, and an annual claim cannot credibly evidence whether the consumer bought renewable energy for those hours or not.

"The current system helped scale renewables but it's no longer sufficient for where we are now. 24/7 hourly matching doesn't break the system, it finishes it."

– JP Cerda, Renewabl's CEO

Killian Daly, Executive Director of EnergyTag and a member of the GHG Protocol's Scope 2 Technical Working Group, argues in EnergyTag's 2025 commentary that hourly matching aligns corporate electricity accounting with how the physical grid actually works.

Feasibility allowances and the timeline most coverage misses

The proposals also include a set of feasibility allowances most coverage skips:

- Load profiles to approximate hourly data where metered data is not available.

- Exemption thresholds for smaller organisations.

- A legacy clause for existing contractual commitments.

- A multi-year phased implementation timeline.

The phased timeline matters. The revised Guidance is expected to publish in late 2027, with adoption phasing in from around 2028. SBTi, CDP, and CSRD will layer their own transition periods on top. The intent is to give buyers time to get the data, the systems, and the procurement design ready – not to force a step-change reporting cycle next year.

.webp)

Sam Kimmins, Director of Energy at Climate Group, set out the position publicly in September 2025: RE100 and the 24/7 CFE Coalition treat the revision as an accounting correction, not an immediate boundary move. The proposed updates tighten the method. They do not move the renewable procurement target.

How Scope 2 emissions are reported today, under the Greenhouse Gas Protocol

Where Scope 2 sits in the Greenhouse Gas Protocol

The Greenhouse Gas Protocol categorises corporate carbon emissions into three scopes. Scope 1 covers direct emissions from sources a company owns or controls – fuel combustion in boilers, vehicles, industrial processes. Scope 3 covers indirect emissions across the supply chain, from raw materials to product end-of-life.

Scope 2 sits between them: the indirect emissions associated with the electricity, steam, heat, or cooling a company purchases. For most corporates, purchased electricity is the dominant Scope 2 emissions source, and the largest piece of the carbon footprint a buyer can move quickly through procurement.

Two methods, used in parallel

Scope 2 emissions reporting runs on two methods, used side by side. The location-based method takes the average emissions of the grid where electricity is consumed. The market-based method uses the buyer's contractual instruments – PPAs, green tariffs, unbundled Energy Attribute Certificates (EACs) – and lets the buyer claim renewable electricity on the strength of an annual volume of certificates, even when the actual hour of consumption was supplied by fossil generation.

Dual reporting stays under the proposed revisions for 2027. What changes is what each method requires, not what they cover:

- The market-based method gets tighter contractual rules.

- The location-based method gets a stricter emission factor hierarchy: spatial boundary first (local grid before national), then temporal granularity (hourly before monthly before annual), then factor type. A factor that reflects the actual mix supplied to your local grid beats a national average, even if the national average is hourly.

The annual matching gap is wider than just unbundled certificates

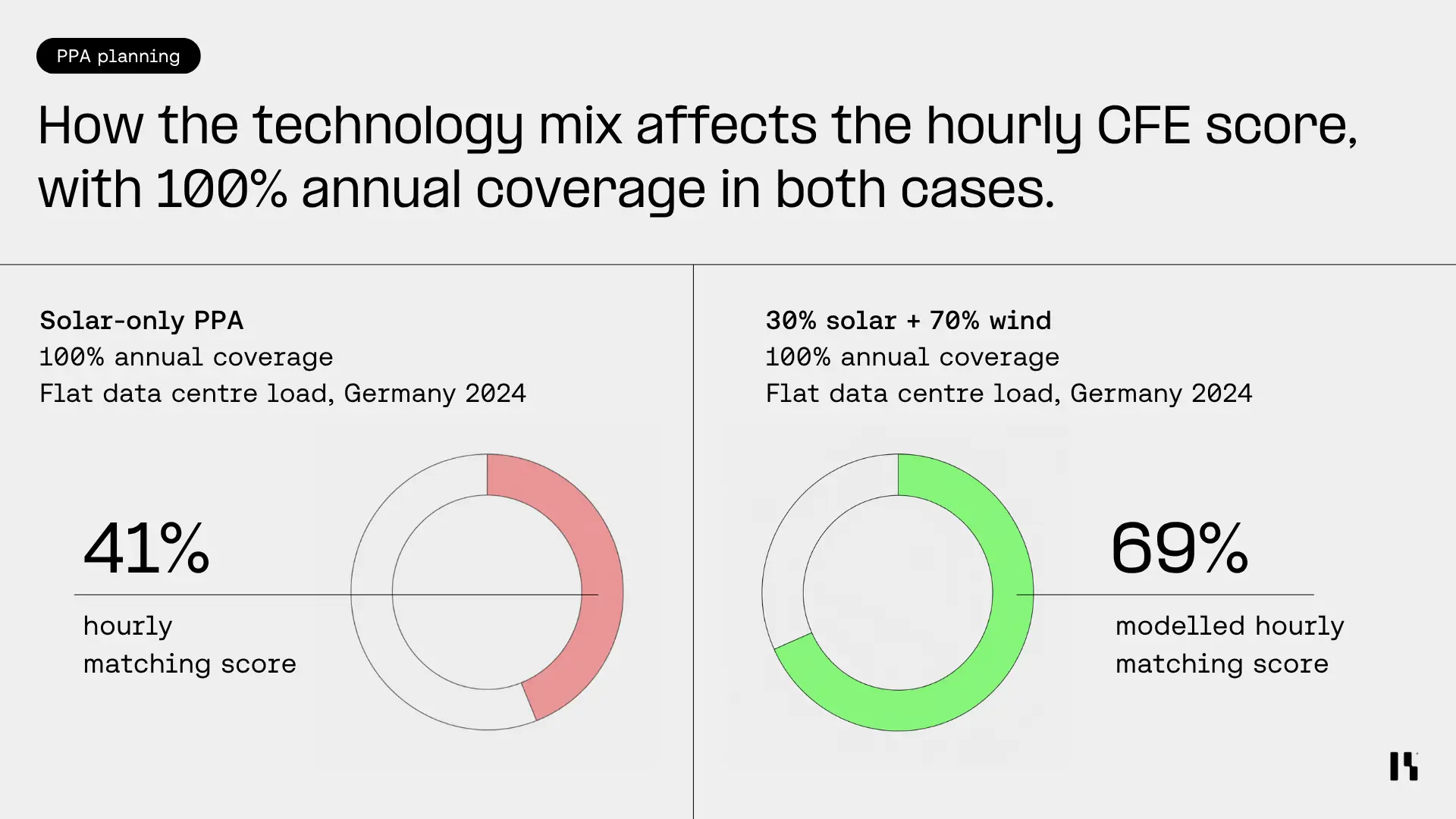

The gap the revision is designed to close is wider than the public conversation usually allows. Annual matching is not a problem unique to unbundled certificates. A company with a solar PPA for 100,000 MWh can have 100 per cent annual coverage and well under 50%on an hourly basis.

Green tariffs work the same way: the supplier pairs grid electricity at the meter with an annual volume of Renewable Energy Credits (RECs) or Guarantees of Origin (GOs)..

The energy procurement instrument does not change the hourly gap. Hourly measurement – paired, where the case fits, with hourly-matched procurement design – is what closes it.

The full mechanics of how the hourly view works as a measurement layer are covered in our hourly renewable energy matching guide.

Why the real blocker is buyers’ data, not the energy products

Most corporate energy buyers manage their renewables across a patchwork of separate platforms – one for procurement, one for certificate management, one for price benchmarking, one for carbon accounting – stitched together with spreadsheets and SharePoint folders.

Sustainability and procurement teams use different files. Data lives in supplier portals, invoice PDFs, and inboxes, but never in one place.

The result is missed certificates and no time left for strategy. Many corporations measure emissions data in spreadsheets, which is inefficient at small scale and breaks at large scale. The revision turns the visibility problem into an internal audit opportunity, before any standard lands.

"You can’t act on what you can’t see."

– Carolyn Addy, Renewabl

What this visibility exposes lands hardest on the buyers who thought they were already done.

In our work with a global manufacturing company, an annual 100 per cent renewable claim dropped to roughly 36 per cent on a proxy-data hourly view in the firm's EU HQ country. The portion that could be evidenced with granular certificates fell further still – a separate gap, driven by missing hourly data rather than by the underlying generation mix.

The reporting was correct under the existing method. The carbon accounting test exposed the gap the existing method allowed.

The 2023 research by Eurelectric and Pexapark demonstrated that without an hourly view, the difference between solar and wind procurement is not always visible to a buyer. Neither is the question of which mix would have closed the gap for a specific load.

Estimate your hourly CFE score before the consultation results land

That gap between annual coverage and hourly coverage is hard to see without the data, and most buyers do not have it lined up yet. Renewabl's free Hourly CFE score estimator gives you a directional version without the need to upload any data.

The model uses three real 2024 load shapes – retail/office, manufacturing, and data centre – and proxy solar and wind generation profiles for the same year, volume-weighted across the 8,760 hours of the year. The output is an estimated hourly CFE score (a good starting point rather than a reportable position).

For corporates waiting on the consultation results, it is a quick read on where current procurement sits before any framework arrives.

Try the Hourly CFE score estimator.

The same data work pays back twice

Hourly data does more than defend a Scope 2 claim. It also shows where a PPA actually hedges the buyer's load – and where it doesn't, making the value of long-term energy purchases more visible.

Shape risk: where your PPA holds and where it doesn't

Shape risk is the gap between when a PPA generates and when the buyer consumes. A 100 MW solar PPA can match annual volume on paper while leaving the buyer exposed every winter evening. On paper, the deal looks hedged. Look at it hour by hour, and the gap shows up.

A 2023 Eurelectric and Pexapark analysis found that a Finnish buyer running a 10 MW baseload PPA could have avoided roughly €14m in 2022 settlement exposure by moving from a 100 per cent annual-matched structure to a 90 per cent hourly-matched one – the shape risk the annual structure had been masking.

Why the same view serves sustainability and procurement

The same data work that defends the renewable claim also tells procurement teams whether an offered PPA reduces price-risk exposure or amplifies it.

"Hourly matching effectiveness is a great proxy for hedging effectiveness."

– Carolyn Addy, Renewabl

On the procurement side, the value sits in clearer pricing signals.

"Hourly procurement provides clearer price signals and more stable revenue across different time periods. It aligns cost with real-world system conditions, rewarding renewable generation when it is most valuable and accelerating investment where it’s needed most."

– JP Cerda, Renewabl

There is a third return that the standard debates rarely reach. Energy sovereignty has become a procurement concern in its own right. Buyers in Europe and beyond are mapping their exposure to imported power – not just on cost but on supply resilience and grid balance.

"You cannot rely solely on traditional and external sources of power, such as imported gas. You must build a more resilient, localised system."

– JP Cerda (Renewabl) for S&P Global, April 2026

With a more granular approach to renewable energy accounting in place, sellers will understand where the market is and build assets closer to where demand exists. Combined with energy storage, this approach will help balance the grid and enhance energy security in the long term.

The market context is sharpening the case. BloombergNEF's 1H 2026 Corporate Energy Market Outlook puts corporate clean-power procurement in 2025 at 55.9 GW, down about 10 per cent year-on-year for the first decline in a decade. The four largest corporate buyers are responsible for roughly half of all activity. Hybrid deals (energy plus storage) accounted for 5.8 GW.

When concentration is that high and volume is softening, procurement teams need a deeper diagnostic on the deals they do sign. Hourly is that diagnostic, even if it’s not driven by climate action or any specific reduction targets.

How to phase the move – annual to monthly to hourly

The standard advice is “start measuring hourly now”. The gating step is data: meter data, supplier data, portfolio consolidation. The hourly score is the output of that work, not the starting point.

For most buyers, the realistic next procurement step may be from annual to monthly alignment, not directly to hourly.

Monthly matching is achievable with the certificate infrastructure already in place, and produces meaningfully more credible claims than annual volume matching. Hourly accountingis not abandoned in that move – it sits underneath as the architecture, ready when the market and the data catch up.

Most buyers can reach 60 to 75 per cent hourly coverage from a combined solar and wind starting position before costs rise sharply. A major European independent power producer we worked with moved from below 40 per cent to over 70 per cent hourly CFE in one country with no meaningful budget change – sequencing the data work first, then re-shaping procurement against the real load profile.

The IEA's 2022 Advancing Decarbonisation through Clean Electricity Procurement – still the most-cited public benchmark, though premiums vary by market and load shape – found that 90 to 95 per cent 24/7 CFE targets carry only a small cost premium over 100 per cent annual renewable matching. That puts the cost question on the back five to ten per cent, not the first sixty.

The three-step adoption path: baseline, design, scale

Three moves, in roughly this order:

- Baseline. Reconcile your energy consumption data against the contracts and certificates you already have, so consumption and supply are on the same hourly basis If your meter data isn't ready yet, use Renewabl’s Hourly CFE score estimator to baseline an hourly CFE score before any framework asks.

- Design. Size the next tender against your actual load shape, not against an annual volume target. Treat monthly alignment as the near-term goal where hourly is not yet feasible.

- Scale. Combine time matching with location matching across markets, business units, and generation technologies, at the granularity each market supports.

There are about 18 months between now and the revised standard's publication. Used well, that window is enough to consolidate your renewables data into one place, baseline a real position you can stand behind, and use that baseline to shape the next tender or renewal.

"First things first: get visibility of your data."

– Carolyn Addy, Renewabl

The buyers who use the next months are giving themselves easier conversations later – with their CFO, their auditors, and their procurement counterparties. The gap just compounds, quietly, until it surfaces in an audit cycle or a renewal.

Renewabl is one platform to track, trade, and report renewables – in one place, replacing the patchwork of separate tools most buyers stitch together today. Hourly matching is built into the architecture, ready for when the standard, the data, and your portfolio are. We help corporates do the data work and shape the procurement that follows.

.webp)

.webp)