JP joined this episode of The Energy Revolution to discuss the evolving role of power purchase agreements (PPAs) in the UK and beyond, from CfDs and corporate demand to hourly matching and the future of data-driven procurement.

In conversation with Sulaiman Ilyas-Jarrett — former senior adviser at the Department for Energy Security and Net Zero and at Number 10, and now a fellow at the University of Cambridge — JP shares his perspective as founder and CEO of Renewabl, a company that uses data and technology to improve how PPAs are structured, analysed and transacted.

Key takeaways

- PPAs and CfDs serve different roles: CfDs drive renewable capacity; PPAs provide corporates with long-term price visibility, volume certainty and credible claims.

- Corporate focus is shifting from additionality to traceability and avoiding greenwashing.

- Regulatory pressure (GHG Protocol Scope 2, SBTi, RE100 24/7) is pushing demand for hourly matching and granular accounting.

- PPA structures are becoming more flexible, aligned with real consumption profiles rather than static baseload contracts.

- The future of PPAs is data-driven, impact-focused and built around 24/7 carbon-free energy principles.

What follows is a very slightly amended transcript of the full episode, edited for clarity and readability.

CfDs and PPAs play different roles in the market

Sulaiman Ilyas-Jarrett: Thank you very much for joining us today, JP. We’re going to be talking about PPAs, the future of private purchasing of power in the UK and beyond. We’ve just had this record CfD auction. A lot of power is effectively being procured by government. Is there a future for power purchase agreements in the UK market?

JP: Yes, well, first of all, thank you so much for having me. It’s great to be here. The role of PPAs will continue to be super important. You’re absolutely correct — CfDs are taking quite a lot of volume — but I think CfDs and PPAs can work alongside each other. They are completely different mechanisms.

The CfD is designed primarily to support volume and increase the amount of renewables, which is exactly what it’s doing. PPAs, on the other hand, are more focused on corporate decarbonisation, providing corporates with price visibility and volume visibility into the future. They play two completely different roles, and I think we need them both.

"I think CfDs and PPAs can work alongside each other."

– JP Cerda, Renewabl

Sulaiman Ilyas-Jarrett: That’s probably a slightly provocative question to start with. I agree there’s a role for both, but it’s something I often get asked: what’s the point of PPAs if CfDs are buying everything anyway? What can PPAs do that buying on the wholesale market or relying on spot prices can’t?

JP: That’s a really good question. What PPAs are really good at is providing corporates with three things. First is price visibility. It’s super important for corporates to understand pricing for the next 5, 10 or 15 years. Second is volume security. Corporates can rely on the output from a specific asset aligned with their needs. Third, with increasing legislative and regulatory pressure around sustainability and accountancy treatments, PPAs provide a very strong mechanism for corporates to make credible claims.

If you’re under legislative pressure, you can rely on PPAs to demonstrate commitment to sustainability. That’s very different from what CfDs are designed to do.

The PPA driver has shifted from additionality to traceability

Sulaiman Ilyas-Jarrett: Has the weighting between those reasons changed? Was it more about corporate social responsibility in the past and now more economic, or has it always been a mix?

JP: It’s always been a mix. From our perspective, it has shifted slightly. Five years ago additionality was a big driver. Corporates wanted new-build assets they could help finance and attach their name to. Now it’s more about claims — avoiding greenwashing and ensuring the energy used genuinely comes from renewable sources.

Additionality still matters, but corporates want traceability. If the asset is operational and traceable to wind or solar, more corporates are satisfied because they can make a verifiable claim. Price volatility and volume security, though, remain constants when signing a PPA.

The energy crisis accelerated structural innovation in PPAs

Sulaiman Ilyas-Jarrett: During the 2020–22 energy crisis, wholesale prices spiked and suddenly there was intense interest in PPAs. Has that left a lasting legacy?

JP: Yes, it has evolved. PPAs are becoming less black and white. Previously it was simple: you either had a PPA or you didn’t. Now structures are evolving — pricing structures, shapes, tenure, and size.

As more assets connect to the grid, there’s greater flexibility. Corporates that couldn’t sign PPAs 10 years ago now can. The structure is more tailored to buyer requirements. You can buy specific shapes, pay-as-produced arrangements, different pricing structures. It’s really exciting.

“PPAs are becoming less black and white. Structures are evolving — pricing structures, shapes, tenure, and size.”

– JP Cerda, Renewabl

Sulaiman Ilyas-Jarrett: Can you explain what you mean by “shape”?

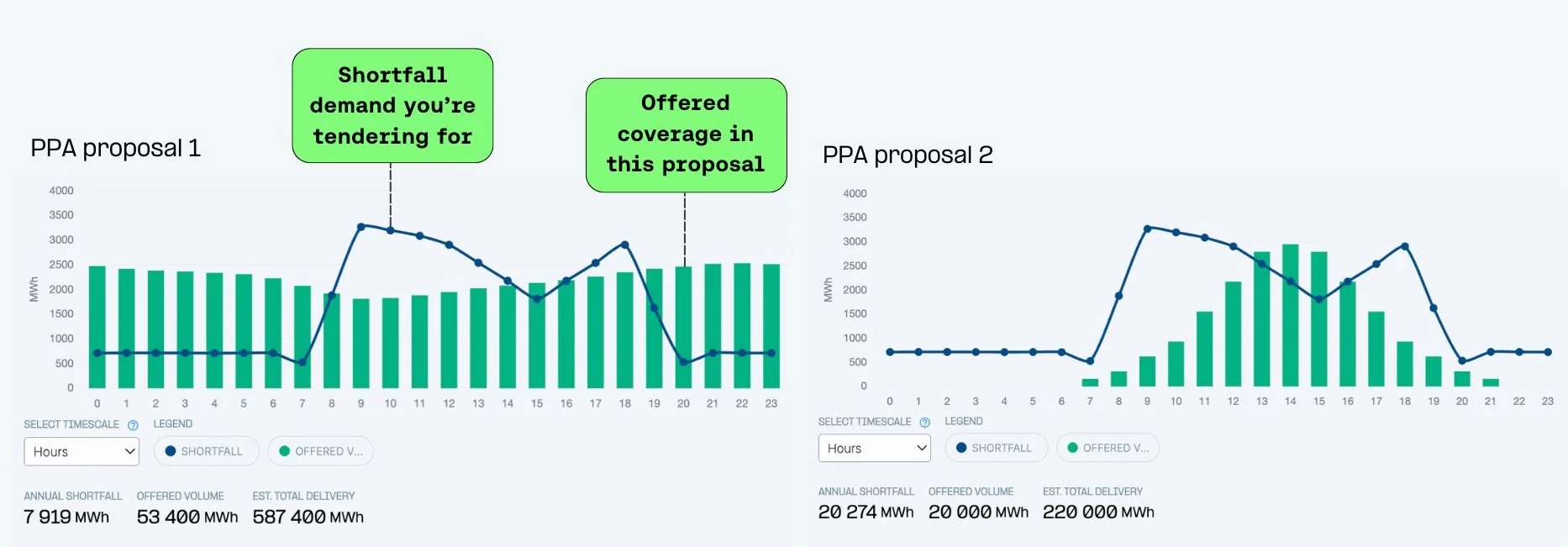

JP: You can buy a solar shape, a wind shape, or baseload. It depends on your consumption profile. Corporates are now under more pressure to understand their demand profile and match it. That’s where hourly matching comes in — understanding when energy is produced and when it’s consumed, and overlaying the two.

If you’re an office open nine to five, a solar shape makes sense. If you’re an industrial company operating 24/7, wind or baseload may fit better. If you buy solar just for price reasons but consume at night, you’re effectively using fossil fuels overnight.

Sulaiman Ilyas-Jarrett: And pay-as-produced?

JP: That simply means you pay for whatever the asset produces at a specific time. It’s reconciled against actual output.

“If you buy solar but consume at night, you’re effectively using fossil fuels overnight.”

– JP Cerda, Renewabl

The PPA market is still highly analogue

Sulaiman Ilyas-Jarrett: You’ve been in PPAs for a long time. What attracted you to this space?

JP: I wanted to create impact. I came from commodities trading, but PPAs allow generators to build more assets by convincing corporates to sign long-term agreements that give them visibility and a hedge. The mechanism itself creates new renewable capacity.

Over time, the journey evolved from CSR-driven to also being about securing power at today’s price. My focus has always been simplifying how these contracts are structured and signed, because they’re long-term and complex, with many risks. But they can be beneficial for corporates if done properly.

“PPAs allow generators to build more assets by convincing corporates to sign long-term agreements.”

– JP Cerda, Renewabl

Sulaiman Ilyas-Jarrett: It can feel very analogue — people at conferences asking if anyone has power plants to sell.

JP: Exactly. I’ve worked on building PPA marketplaces, but it’s not as simple as adding to cart and checking out. There’s complex negotiation around price, volume, tenure and risk allocation. That process can take months.

One of the big issues is price validity. After months of negotiation, the seller may say the price is no longer valid. Then the corporate’s budget doesn’t fit, and time is wasted. Technology can help close that gap by firming up price, volume and tenure earlier in the process.

Sulaiman Ilyas-Jarrett: You once reduced timelines to six months from an average of two years. Can it go faster?

JP: With better data visibility and digital tools, yes. If corporates can understand net present value, volumetric exposure, price exposure and long-term forecasts more clearly, decisions can be made faster.

If corporates can understand net present value, volumetric exposure, price exposure and long-term forecasts more clearly, [PPA] decisions can be made faster.

– JP Cerda, Renewabl

Forecasting power prices remains extremely difficult

Sulaiman Ilyas-Jarrett: During the crisis, producers sometimes preferred to stay in the spot market rather than lock in prices. How do you forecast price in such volatile markets?

JP: We’re not very good at forecasting. I remember advising a telecom company when PPA prices were around £40/MWh. A reputable forecast suggested prices might fall to £20 or £10. They didn’t sign. That never happened.

Renewables are still relatively new in terms of data history. There are too many fundamentals — pandemics, wars, fuel mix changes. It’s difficult to predict.

“There are too many fundamentals — pandemics, wars, fuel mix changes.”

– JP Cerda, Renewabl

With high solar penetration and negative pricing events in Europe, predicting becomes even more complex. Governments are now taking capacity, batteries and curtailment more seriously, but the system is still evolving.

CfDs reduce asset availability for corporate PPAs

Sulaiman Ilyas-Jarrett: CfDs can influence PPA markets too. If CfD prices are attractive, fewer assets are available privately.

JP: Yes. In the UK especially, it benefits sellers. Good CfD prices and long tenures make it easy to opt in. That reduces asset availability for corporate PPAs.

But corporate demand will continue to grow because legislation is catching up — Greenhouse Gas Protocol Scope 2 updates, SBTi version two, RE100’s 24/7 coalition. Regulatory pressure will increase corporate demand. Both mechanisms are needed. It’s about balance.

The next phase of PPAs is technology-driven and hourly

Sulaiman Ilyas-Jarrett: Let’s talk about hourly matching and data.

JP: The first phase of PPAs was contractual. The next phase is technology-driven. Assets produce power hourly. Corporates need to understand consumption profiles hourly. You overlay production and consumption to see excesses and shortfalls.

Historically corporates matched annually. Now granularity matters because renewables are intermittent. With demand expected to increase significantly, visibility becomes crucial.

"The first phase of PPAs was contractual. The next phase is technology-driven."

– JP Cerda, Renewabl

Sulaiman Ilyas-Jarrett: Are we technically ready for full 24/7 matching?

JP: Not fully. Many existing PPAs weren’t structured hourly. Issuing systems need to evolve — for example, Ofgem currently issues certificates per megawatt hour, not per hour. Hourly certificates would be required for true matching.

Transmission, distribution, and regulatory systems need to evolve. We’re not there yet, but it’s being taken seriously.

Sulaiman Ilyas-Jarrett: Location matters too, but zonal pricing hasn’t been adopted in the UK.

JP: Time-based matching is the first step. Location-based may follow. Encouraging corporates to source energy locally makes sense. That could drive more impactful procurement in the future.

The future of PPAs is about real impact, not tick-box compliance

Sulaiman Ilyas-Jarrett: Finally, what excites you most about the future of PPAs?

JP: The move from tick-box compliance to impact. Hourly matching and better data make corporates think more deeply about their procurement. Technology enables better decisions — measuring carbon content hourly, analysing imports and exports. That’s what excites me most.

Sulaiman Ilyas-Jarrett: Thank you so much for coming.

JP: Thank you for having me.

Thank you for listening to the Energy Revolution podcast. If you’ve enjoyed today’s episode, subscribe for weekly conversations exploring the most fascinating questions in energy. Share it with colleagues, friends, or anyone energy-curious. We look forward to the next episode.

.webp)