%20(1).webp)

Signing a renewable Power Purchase Agreement (PPA) used to look like a clean win on price and carbon. In renewable-heavy markets, it has become more complicated. As more solar and wind come online, clean power increasingly floods the same hours. This is dragging wholesale prices down, sometimes below zero, just when contracted output is at its highest. The hedge a buyer thought they had starts to behave differently.

Annual procurement masks a surprising amount of residual market exposure, because a renewable PPA only hedges the hours it actually covers. As renewable penetration rises, the uncovered hours are where the risk lives.

Key takeaways

- A renewable PPA only hedges the hours when the project is actually generating. The uncovered hours, where there is no generation, can leave buyers exposed to volatile spot-market prices.

- As companies move from traditional supply contracts – fixed-price or flexible deals where the supplier manages timing – to corporate PPAs, they take on more shape, balancing and timing risks.

- Corporates with 90–100% annual coverage often sit at just 40–50% on an hourly basis. The rest is exposed to spot prices.

- Hourly matching, widely discussed as a sustainability measure, is also a practical proxy for how well a PPA hedges: match 80% of your demand hour by hour and you have an effective hedge for about 80% of your volume.

What is power purchase agreement hedging?

Let’s start with what a PPA hedge is not. A common misconception is that a power purchase agreement should earn you money – it shouldn’t.

A PPA hedges price: it trades the risk of volatile spot prices for a known, fixed price over the long term. In a high-price year you are protected. In a low-price year you may pay more than the market, sometimes called being "out of the money". That trade, stability and predictability in exchange for giving up the upside, is the point.

In accounting terms, hedge effectiveness is how well the hedging instrument (here, the PPA) offsets changes in the thing being hedged, which is your exposure to volatile electricity spot prices.

“The main role of a PPA hedge is to protect you when markets go high. The higher your hedge effectiveness, the more of that volatility is covered.”

– Paul Hill, Renewabl’s Head of Energy Markets

A hedge works by securing the volume you need at a fixed price. Electricity settles hour by hour, so the hedge only holds in the periods where your hourly demand coincides with the hourly hedge generation volume.

In the hours you don’t have hedge coverage, you must buy the shortfall, in hours where you have an excess of hedged supply volume, you must sell the excess at the prevailing market price. In both instances the hedge is not optimised for those hours (either unhedged or over-hedged) and therefore you are exposed to market price volatility.

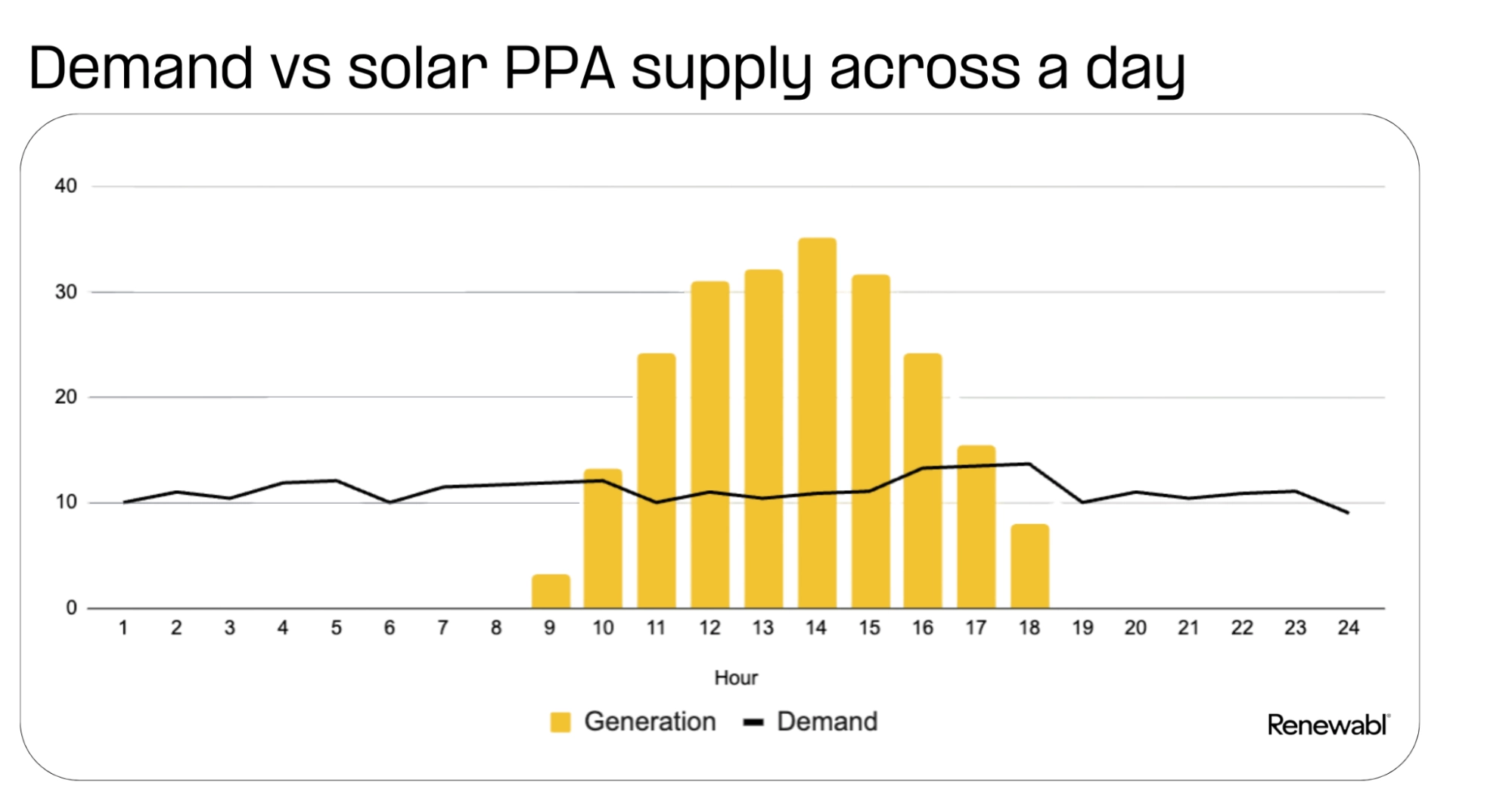

In this example a chart is used to visualise:

- A corporate buyer’s typical daily demand profile

- The corporate buyer’s contracted Solar PPA (the hedging instrument)

Across 24 hours, supply and demand are volumetrically matched. However, at an hourly level, they mis-match in most hours:

- No supply in off-peak hours

- Oversupply in peak hours

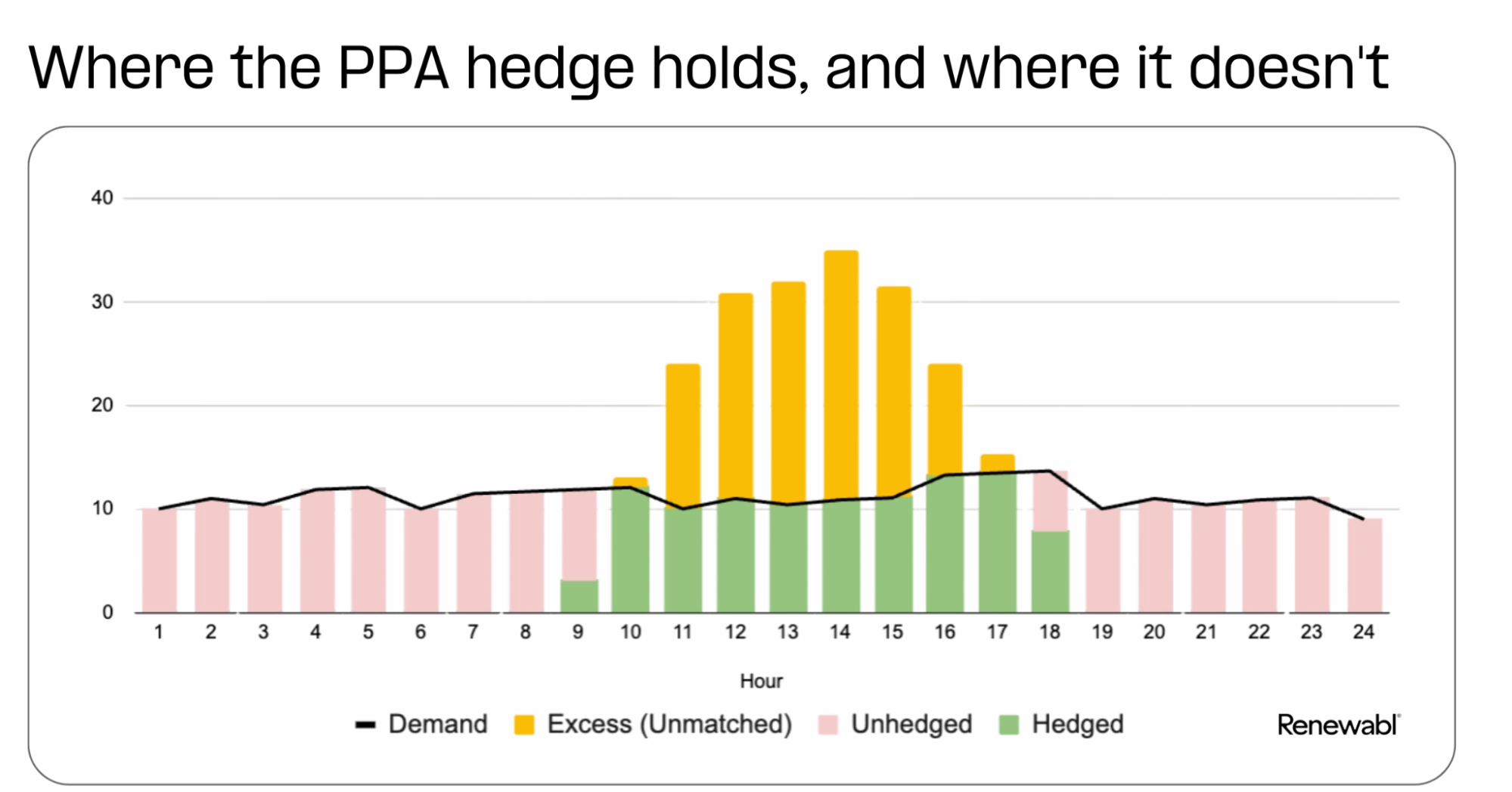

The next chart shows the same data, categorised to highlight, and quantify, the mis-match between supply and demand.

- Hedged electricity demand (38.37% of total demand) – demand volume matched with supply, so the price hedge is effective.

- Unhedged electricity demand (61.63% of total demand) – demand volume not matched with supply, so it is exposed to spot pricing.

- Excess (over-hedged) electricity supply (52.45% of total supply) – supply volume above the buyer’s need. This volume must be sold back to the spot market, so it can create losses if the sell-back price is below the PPA strike price.

When PPA risk shifts from supplier to buyer

Under traditional fixed-price and flexible supply contracts, large energy buyers had a straightforward arrangement. The supplier sourced, balanced and delivered power that followed their consumption through the day. Your supplier would provide generous contractual volume tolerances. So if demand spiked, the supplier found more power; if it fell, the supplier absorbed the surplus. Buyers paid for electricity when they used it, without thinking much about when or where it came from. The supplier carried most of the timing risk inherent in electricity markets.

Corporate PPAs changed that. Firms gained long-term renewable sourcing and protection against future price inflation, but took on risks the supplier used to manage in the background.

A PPA often does not entirely replace a supply contract; it supplements it, covering part of your volume while a supplier still balances the rest. Instead of buying electricity that follows demand, you contract electricity that arrives when the asset generates. A solar project produces most of its output around midday, regardless of when you actually need power.

That creates a new set of considerations:

- topping up when renewable generation is low

- managing any surplus delivered when generation exceeds demand

- pricing the gap between when the asset generates and when you use power

The shift is temporal. When electricity is no longer hedged on an annual volume basis, you are exposed to the hourly structure of generation and demand. A PPA can protect against broad market price movements while still leaving you exposed to volume shortfalls, to timing mismatches between generation and demand, and to the price the asset captures when it generates. A solar PPA can hedge midday prices well while leaving morning ramps, evening peaks and overnight demand fully exposed.

Hedging with physical vs financial PPAs

PPAs come in two main forms, and both hedge price.

- Under a physical PPA, an agreed volume of clean power is delivered to you, often sleeved through a supplier, at a fixed price.

- Under a financial or virtual PPA (vPPA), no power changes hands: you keep buying from the market and financially settle the difference between an agreed strike price and the wholesale price.

Either way you fix a price for contracted volume. The dynamics in this article, selling excess back to the market and topping up uncovered hours, show up most clearly in as-produced and financial structures, where settlement follows the asset’s hourly output.

Double exposure

An analogy to make the mismatch concrete: picture a warehouse manager who strikes a deal with an ethically sourced caterer to supply discounted meals for the team. Healthy and affordable. Then it turns out the caterer can only send a truck at midday. Workers on the evening shift have to look elsewhere. Worse, sometimes the truck doesn’t have enough food on hand; other times it has too much.

Standalone solar PPAs work much the same way. They can potentially leave buyers over-hedged in midday hours and completely unhedged in mornings, evenings and nights, if not sized correctly.

This is becoming more visible as renewable penetration rises across Europe. Solar increasingly generates into periods of oversupply and depressed prices. In April 2026, solar capture factors (the share of the average market price a solar asset earns when it generates) fell sharply: to around 0.10 in France, down about 75% year on year, with similar pressure in Germany and Italy, as negative-price hours surged.

“[In some markets], there’s no point building more standalone solar because there’s already an excess of solar supply. Instead we are seeing a pivot from developers towards technology diversification as well as a stronger focus on storage”

– JP Cerda, Renewabl’s CEO

That doesn’t make solar PPAs worthless. It means the nature of renewable procurement risk has changed.

Capture risk: pricing a temporal mismatch

This shows up most in as-produced PPAs, where generation follows the natural output of the asset. During strong solar hours you may receive more power than you can use, and the excess is sold back into the market, sometimes at weak or negative prices. At the same time, you may still buy uncovered power through expensive evening hours once solar drops off.

The result is double exposure: under-hedged when prices are high, over-supplied when they are low.

Utilities and traders know this problem well. Many now offer shaping services that turn intermittent generation into flatter, baseload-style supply, for an added fee which materially increases the effective strike price. A baseload PPA goes a step further: the generator commits to deliver a set volume in each period and takes on the volume risk itself, again at a price.

Two PPAs with the same annual volume can carry very different exposure. If budget certainty is the goal, annual volume is the wrong lens for measuring it.

Hourly matching is more than a sustainability metric

Hourly matching, measuring clean energy supply against demand hour by hour, is usually framed as a sustainability tool and the basis for 24/7 carbon-free energy (CFE) claims. In renewable-heavy markets, it is also a way to read the strength of a PPA hedge.

A company’s hourly CFE score is the share of its electricity demand matched to carbon-free generation hour by hour. The same number has a financial read: it tells you volumetrically how much of your load is actually hedged. If you are 80% hourly matched over a period, you have an effective hedge for about 80% of your volume; the remaining 20% is exposed to market prices.

Eurelectric’s analysis with Pexapark points the same way: the more of your demand you match hour by hour, the greater the hedging benefit. In one example, a Finnish consumer on 10 MW of baseload power could have saved over €14m in 2022 with a 90%-hourly-matched PPA combining solar, wind and storage.

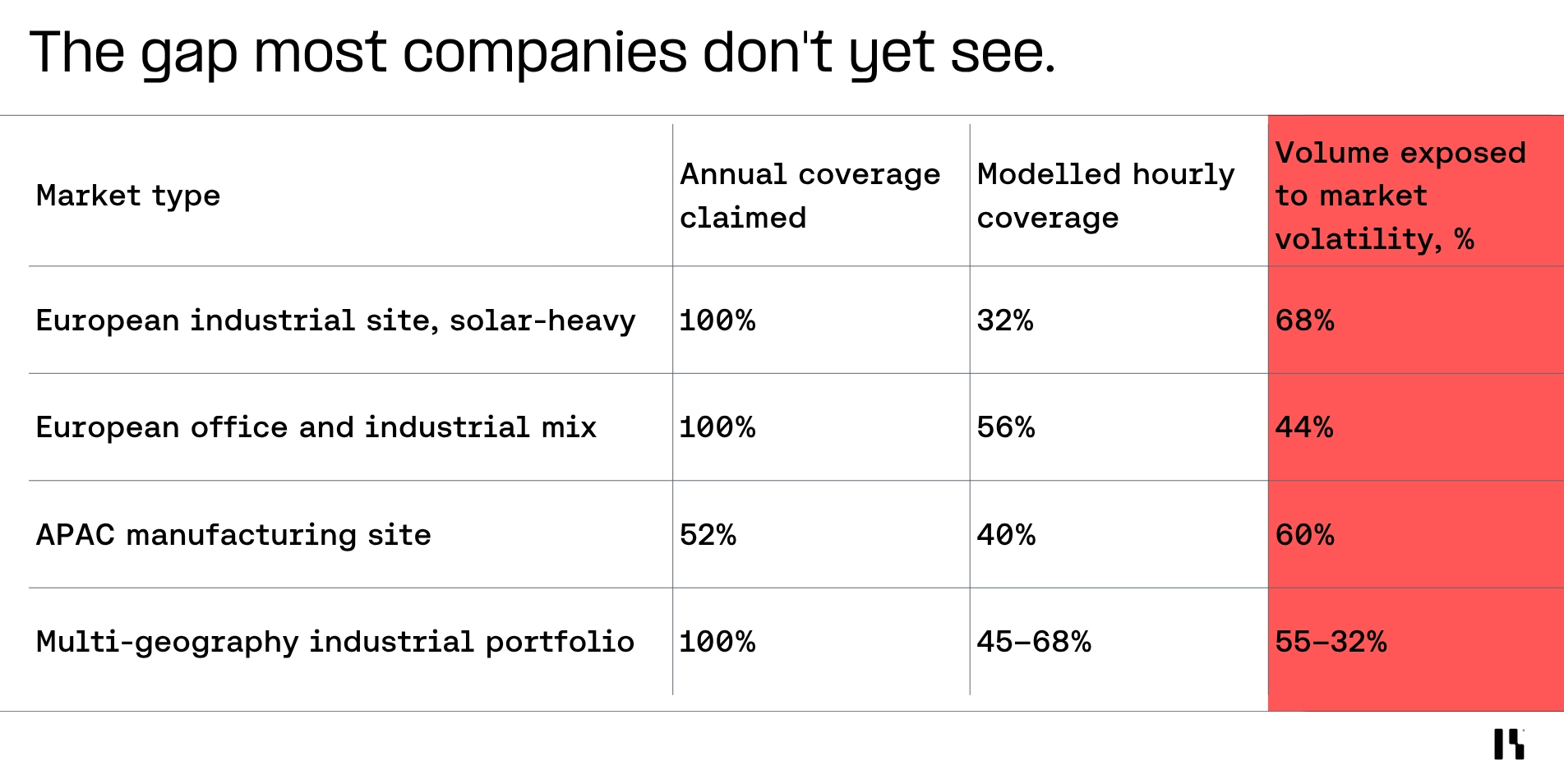

It also exposes the gap most buyers can’t see. Corporates with 90–100% annual coverage often sit at just 40–50% on an hourly basis.

“The same hourly view that supports a stronger Scope 2 claim also helps you build a more resilient portfolio.”

– Carolyn Addy, Renewabl’s Head of Commercial

None of this is all-or-nothing. For many buyers the right first move may be annual to monthly, with hourly as the direction of travel rather than a standard to hit now. Existing PPAs and renewable energy certificates still count, and a baseline is a shared reference point for finance, procurement and sustainability, not a verdict. You can find a starting score with Renewabl’s CFE score estimator.

What we see buyers checking before signing a PPA

Before signing or renewing a power purchase agreement, the buyers we see getting this right look past annual generation volumes and model their hourly exposure directly. Calculations start by comparing actual load profile against the asset’s expected generation profile, and ask:

- Which hours are covered?

- Which hours stay exposed?

- How much excess generation is expected?

- What happens during winter peaks or low-renewable periods?

- What is the settlement structure?

Once those questions are answered, negative-price clauses deserve a close read, especially where renewable penetration is rising and negative-price hours are becoming more common. The clause sets who carries the cost when wholesale prices fall below zero: whether you keep paying the strike price on all contracted volume, or the contract limits the downside with a price floor (often €0/MWh) or lets the generator curtail.

Geography feeds in as well. A PPA that settles in a different market from the one your sites draw from can leave you with basis risk, because the price it pays out against may move differently from the price you actually pay. Congestion and locational price differences within a single market can erode hedge performance the same way. Counterparty resilience carries more weight on longer terms too, since the deal only protects you if the seller is still standing in year 10 or 15.

More firms now stress-test their agreements against different price environments, capture rates, renewable penetration and load conditions. Together, these checks give a clearer picture of the exposure that remains even after the hedge is in place.

“Hourly-matching analysis surfaces which hours are exposed, which technologies and locations actually cover them, and where storage or additional contracts deliver the most hedge effectiveness per euro spent.”

– Paul Hill, Head of Energy Markets at Renewabl

PPA risk doesn’t end with a signature

It is tempting to treat a PPA as done once it is signed, but a hedge that looks effective on day one can dilute over time, even with no change to the contract. Load profiles shift as operations change. New renewable energy projects come online in the regions where your sites sit, reshaping local prices.

The teams we see managing these contracts most effectively tend to track a few signals over time:

- hourly matching performance

- uncovered volumes

- excess generation

- residual spot-market exposure

Treat exposure as fluid. Watching these signals puts you in a better position to adjust hedging strategy when conditions change.

How Renewabl can help

Renewabl is one platform to track, trade and report renewables through an hourly lens.

Renewabl Track compares PPA-contracted generation against your actual demand, hour by hour, so you can see exposed periods and how hedge performance changes over time.

Renewabl Trade brings the same view to procurement. When you run a tender, you can compare proposals on how different PPA structures and technologies fit your demand profile, not just on annual volume or headline price, where differing structures and price-area basis can make two offers look more alike than they are.

Digital Advisory supports teams starting out, with data readiness, procurement strategy and technology choices.

The next procurement question

Plenty of companies still judge PPAs on annual volume and headline savings. In renewable-heavy markets, where timing drives price, that leaves real exposure out of view.

The good news is that it is measurable. Ask how much power is hedged, then go a step further: compare the generation profile in the contract against your actual hourly demand. You can then see which hours are protected and which still ride the spot market.

That is the baseline. From there, the gap closes step by step, starting with the data you already hold.

.webp)