Operational Power Purchase Agreements bring a better risk profile, competitive costs, and reduced contracting complexity. As the greenfield market slows, are they the more practical route for corporate procurement?

The corporate PPA (cPPA) market in the EU contracted sharply in Q1 2026, with volumes down nearly 50% year-on-year to just over 3 GW (S&P Global European PPA Market Overview, Q1 2026). The European cPPA market has traditionally been dominated by additionality-focused buyers keen to lock in long-term PPAs with greenfield (new build) assets. However, we are now seeing corporates increasingly lean on PPAs as a risk management tool rather than purely to deliver on sustainability ambitions. Operational PPAs are central to meeting this growing need.

Key takeaways:

- Demand for operational PPAs is rising as the greenfield market slows: buyers prioritise hedging and price certainty, and older subsidised assets come off support and look for new offtake.

- Operational PPAs typically carry lower risk, shorter tenors (three to seven years) and pricing closer to wholesale, with simpler, faster contracts.

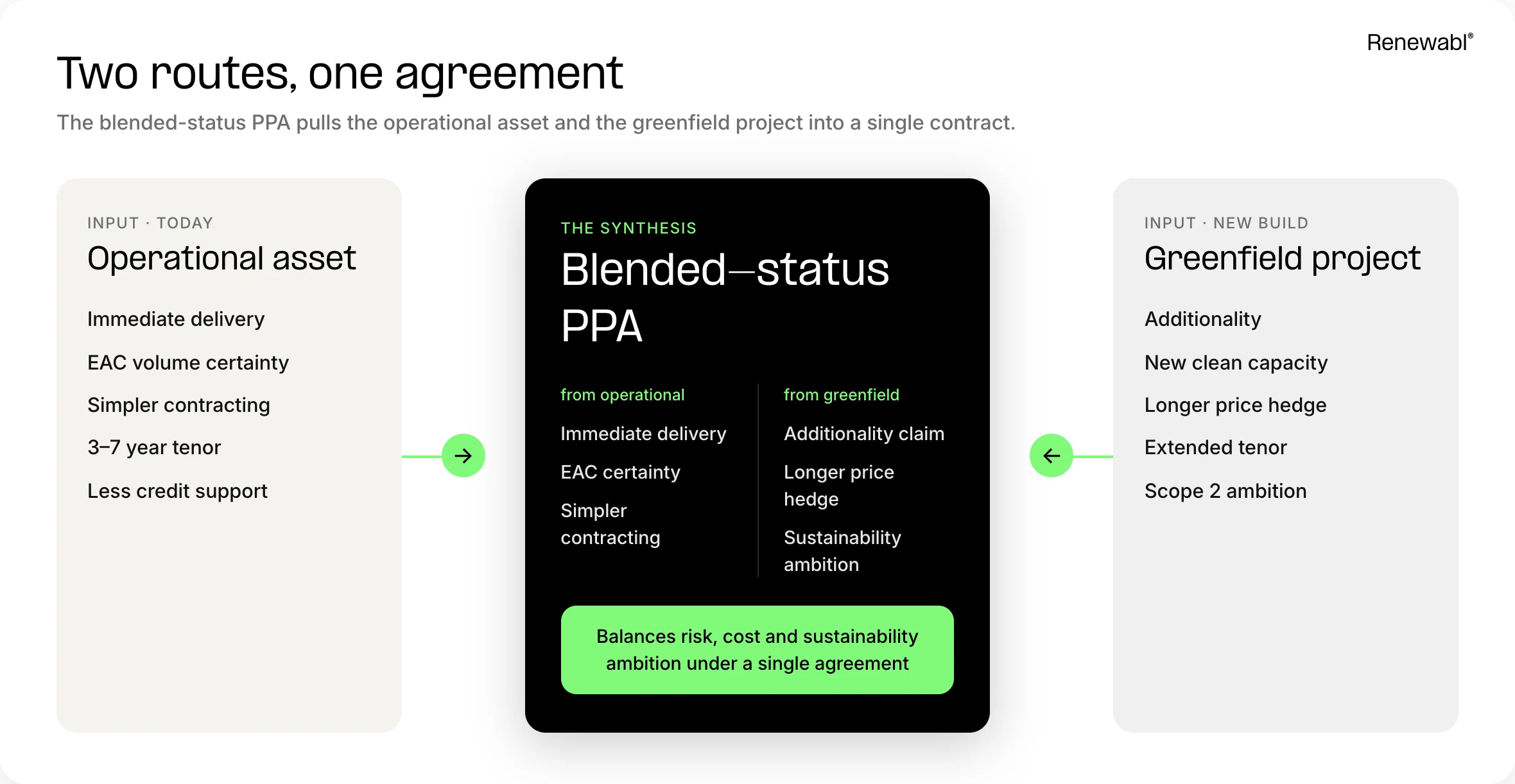

- It is not either/or: a blended-status PPA combines operational and greenfield offtake under one contract, balancing near-term cost certainty with additionality.

What is an operational PPA?

An operational PPA is an electricity supply agreement between an electricity generator and an offtaker (who is using energy) on an asset which is already built and generating power. They offer a more appealing investment opportunity compared to greenfield PPAs as they offer more flexibility on start dates and tenors, lower production and profile uncertainty, reduced construction, permitting and regulatory risks and, subsequently, are often priced closer to prevailing electricity wholesale markets.

What is a blended-status PPA?

A blended-status Power Purchase Agreement combines offtake from an operational asset and a greenfield (new build) asset under one contract. This is different from a technology hybrid PPA, which blends generation types such as wind and solar, or generation with storage. Here the blend is asset status: operational for near-term price certainty, greenfield for additionality.

Drivers for the rise of operational PPAs

This structural market shift is driven by both supply and demand, with both sides converging on operational PPAs as the optimal solution for generators and offtakers alike. Some key market drivers include:

For some markets, more capacity is not the solution

On our grids every day, renewable energy projects are being curtailed significantly and there is substantial price cannibalisation. For example, in Germany, the number of negative-price hours from April 2025 to April 2026 increased by 65% (Pexapark, 2026), and in Spain a 148% increase was observed from February 2025 to February 2026, demonstrating that this is no longer a summer solar issue. In these markets, corporate investment in flexibility may be more beneficial, which aligns with what is being seen in grid connection approvals. As stated by the Executive Director of EnergyTag, Killian Daly:

"In mature markets like Germany and Spain, another solar PPA does not solve the problem. It adds power at hours already saturated with it. What these grids need is flexibility and not more midday generation. The same logic applies to the buyer – a solar-only PPA hedges you at noon, when prices are lowest, and leaves you exposed in the evening, when they spike. Add a battery and the hedge works when you actually need it. Hybridisation is now king."

– Killian Daly, EnergyTag

Immediate hedging against price volatility

In light of the energy market volatility seen in both 2022 and 2026, many buyers’ annual budgets were exhausted in a matter of months. Buyers are under growing stakeholder pressure to secure energy supply that prioritises hedge effectiveness and price certainty. This is not a nice-to-have – it is an immediate need, which feeds directly into the next driver.

Read more about hedge effectiveness in our explainer.

Pace

Many corporates are now within four years of their 2030 net zero commitments. There may simply be not enough time to wait for a greenfield project to reach commercial operation – or to spend six to nine months obtaining approvals for and negotiating a lengthy PPA contract.

An increase in asset availability

Operational PPAs were not broadly considered by corporate offtakers until recently – they simply were not available. That is changing. Renewable capacity built under early subsidy schemes is now reaching the end of its support window. In Germany, EEG feed-in tariffs introduced in 2000 ran for 20 years, so the first assets came off subsidy in 2021 – roughly 16 GW of onshore wind rolling off by 2025 (Clean Energy Wire). As these windows close across the UK's Renewables Obligation, Germany's EEG and Spain's RECORE, generators are looking for alternative refinancing solutions.

This wind-heavy supply pool is also useful for buyers building an hourly-matched portfolio: wind's flatter generation profile scores far higher on an hourly CFE basis than solar at the same annual coverage (Renewabl's CFE score estimator: 75–78% hourly match for wind-only portfolios versus 41–44% for solar-only). For RE100 members, the caveat is asset age: RE100's technical criteria require at least 85% of claimed renewable electricity from assets commissioned or repowered within the preceding 15 years. That doesn't undercut the hourly-matching or hedging case for using them, including as preparation for the proposed GHG Protocol Scope 2 changes. It's a separate additionality/RE100 eligibility question buyers should check alongside it.

Price competitiveness

Renewable power at scale is cheaper than gas. However, traditional corporate PPAs have not always been able to compete with market forecasts, because the additionality premium pushes prices up. Operational PPAs carry a lower risk profile for both generator and buyer, and therefore offer significantly better price points – ones that can genuinely compete with market alternatives.

In Europe, the data points in the same direction. In H1 2025, utility PPA volumes doubled year-on-year to 1.8 GW across 28 deals, while corporate PPA volumes fell more than 40% over the same period to around 4.3 GW (Pexapark, H1 2025). The divergence reflects both the structural shift toward shorter-tenor, lower-complexity contracts and the growing role of utilities in absorbing operational asset offtake.

Comparing greenfield and operational PPAs: key characteristics

Making the case for procuring operational assets

The blended-status PPA: combining operational and greenfield offtake

The decision does not always have to be binary. A technology hybrid PPA blends two or more technology types (wind + solar, solar + BESS) to increase hourly matching and improve hedge effectiveness. A blended-status PPA applies the same logic to asset status, answering the finance team and the sustainability team at once: near-term price certainty from the operational asset, and additionality from the greenfield asset. Through this structure, corporates can balance risk, cost, and sustainability ambitions under one contract.

The evolution of the corporate PPA structure

The European corporate PPA market has undergone a significant structural shift over the past decade, evolving across a wider range of structures and counterparties. Early deals were defined by single-technology, greenfield structures, with corporates signing long-term contracts of 10 to 20 years with a power producer for solar or wind alone, accepting high construction risk in exchange for additionality credentials.

As the market matured, buyers began demanding more from their PPAs: technology hybrid structures emerged, pairing solar with wind or storage to improve generation shape and better match corporate load profiles, though tenors remained long and COD risk stayed elevated. The next inflection point came as corporates became more cost and risk-conscious, turning to operational single-technology PPAs, where assets are already generating power, construction risk disappears, and contract lengths compress to three to seven years.

Today, the most sophisticated buyers are transacting blended-status PPAs, toggling across both technology type and asset status to optimize their portfolios and procurement around their core business rather than becoming power traders, combining operational and greenfield assets in a single structure.

Key contractual differences of an operational PPA

Simpler contracts, faster execution

- Negative price and balancing provisions are often more pragmatically negotiated with hybrid risk sharing approaches as historic negative pricing data is available for an operational asset. Some example hybrid risk sharing structures becoming increasingly popular, include, more specific caps on the number of negative pricing hours integrating seasonality as a factor, price thresholds, time-of-day allocation.

- Conditions Precedents (CPs) are minimal for operational PPAs, due to the reduced COD and construction risk, whereby CPs are often limited to confirmation of grid connection/metered data, sleeving arrangements (if physical PPA). These CPs can typically be satisfied within a week of signing, whereas for greenfield PPAs the CP period can run for 6-18 months.

- Termination clauses are simpler in operational PPAs due to the COD risk being removed, liquidated damages generally reference the cost of sourcing a different asset for supply (if the generator can facilitate this), or the cost of sourcing from the spot market. Comparatively, in greenfield PPAs, the potential liability is greater.

“There’s little doubt that executing a PPA for an operational asset rather than one in development or construction can be both faster and simpler. Time spent negotiating commissioning date protections, delay damages, longstops and certain termination rights can be avoided, and time and costs can be saved by focussing on the key commercial principles of buying and selling power. Ultimately, cutting the time spent going to and fro on corporate PPAs is everyone’s best interests”.

– Chris Pritchett, Partner and Co-Head (Energy & Infrastructure) at Shoosmiths

Monetising operational renewable energy assets: the options

For generators with operational assets, there are three clear financing options for existing assets, and generators are increasingly choosing between routes that participate differently in renewable energy trading and energy markets:

- Go merchant – sell the electricity and energy attribute certificates (EACs), on the volatile wholesale market, where electricity from renewable energy sources is bought and sold across exchanges, platforms and markets to balance supply and demand efficiently. his introduces risk of significant upside and downside price swings, and this price uncertainty is typically not welcomed..

- Sign an operational PPA – find a corporate or utility offtaker, which can sit alongside a generator’s core business to produce energy and sell power from existing assets. Depending on the price and delivery structure, PPAs are an effective mechanism in minimising price uncertainty for generators (compared to the wholesale market).

- Return to government support mechanisms. In some markets, governments offer financing schemes such as Contract for Difference for operational assets to support generators in obtaining price certainty e.g. the proposed wholesale CfD in the UK. These schemes offer multiple benefits for generators, being generally long-term with a fixed, inflation-indexed strike price and a government-backed counterparty.

The key decision-making criteria for generators are risk-cost optimisation, environmental considerations, and the importance of price certainty. For most generators the answer will lie in diversification – either at portfolio level (committing entire assets to different financing mechanisms) or at asset level (for example, 80% offtake via a utility PPA and 20% sold into the wholesale market).

For smaller generators, government schemes offer the lowest friction route optimised for both risk and cost. The standardised terms, sovereign counterparty, and long tenor also remove much of the commercial complexity that a PPA demands. Where auction rounds are unavailable, PPAs offer the most accessible next step, with the decision between corporate and utility depending on offtaker availability, willingness to pay and commercial resource for negotiation.

Ultimately, the generators best placed to adapt will be those who treat their financing strategy as dynamic rather than fixed, revisiting it as market conditions, policy frameworks, and portfolio composition evolve.

Future outlook and trends

The European corporate PPA market is at an inflection point. Contracted volumes have fallen sharply – down around 50% year-on-year in Q1 2026. However, early signals point to increasing corporate interest in PPAs as a price hedging mechanism, and operational structures are increasingly practical to deploy as more assets come off subsidy.

For buyers, operational assets remain an underutilised procurement route. As corporates face pressure to move faster on net zero, and the cost premium and construction risk of greenfield PPAs become harder to justify, operational structures are increasingly the more practical option, helping buyers advance renewable energy targets faster, not just hedge prices. Structured advisory and digital tools – such as Renewabl’s platform – can help corporates baseline their current CFE position and run competitive tenders across greenfield, operational, and blended-status structures from a single workflow.

The decision for corporates does not have to be binary. The blended-status PPA – combining offtake from an operational asset with a greenfield project under a single agreement – allows corporates to balance near-term price certainty with longer-term additionality ambitions. This flexibility is a significant opportunity for buyers who need to satisfy both finance and sustainability stakeholders and is one we expect to see it grow as procurement teams grow more comfortable running structured, multi-source tenders.

"Corporates don't have to choose between price certainty from an operational asset and additionality from a new-build one – in mature markets, both can be procured in the same contract."

– Ruby Tebbutt, Renewabl

For sellers, growing corporate interest in operational PPAs will add competitive tension to a market traditionally dominated by major utilities. The offtake strategy will depend on portfolio size, risk appetite, and access to trading capability, with those demonstrating diversified route-to-market and agility best placed to manage risk and cost.

Looking ahead, two questions stand out: first, how operational PPA pricing evolves relative to utility PPAs and government subsidy schemes such as the proposed UK wholesale CfD; and second, whether the secondary market succeeds in attracting corporate buyers who previously found greenfield structures too complex or too slow. If it does, the corporate PPA market could regain momentum – bringing new private capital into the energy transition at a time when it is most needed, while helping businesses demonstrate environmental leadership and strengthen their credentials among consumers and employees.